43 pricing zero coupon bonds

Zero Coupon Bond: Definition, Formula & Example - Video ... The basic method for calculating a zero coupon bond's price is a simplification of the present value (PV) formula. The formula is price = M / (1 + i )^ n where: M = maturity value or face value i =... What is a Zero Coupon Bond? Who Should Invest? | Scripbox Zero coupon bonds are fixed income securities that don't pay any interest. At the time of maturity, the investor is paid the face value or par value. These bonds come with 10-15 years maturity. Hence, they trade at a deep discount. The bond pricing varies with time to maturity.

How to Calculate a Zero Coupon Bond Price | Double Entry ... The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816)

Pricing zero coupon bonds

(PDF) Pricing of Zero-coupon and Coupon Cat Bonds For instance, Burnecki and Kukla (2003) consider the prices of a zero-coupon and coupon catastrophe bond in the compound doubly stochastic Poisson model. Lee and Yu (2007) investigate a ... Pricing of zero-coupon bond options - Big Chemical ... Pricing of zero-coupon bond options. Starting from the risk-neutral bond price dynamics (5.4), we derive the well known closed-form solution for the price of a zero-coupon bond option. Thus, as shown in section (2.1) the price of a call option on a discount bond is given by [Pg.44] the abiUty to derive a closed-form of t z) crucially depends on ... Zero-Coupon Bond: Formula and Excel Calculator To calculate the price of a zero-coupon bond - i.e. the present value (PV) - the first step is to find the bond's future value (FV), which is most often $1,000. The next step is to add the yield-to-maturity (YTM) to one and then raise it to the power of the number of compounding periods.

Pricing zero coupon bonds. Zero Coupon Bond Calculator - What is the Market Price ... The zero coupon bond price formula is: \frac{P}{(1+r)^t} where: P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding Pricing a Zero-Coupon Bond - PyAbacus Pricing a Zero-Coupon Bond. Fecha: 14 septiembre, 2016 Autor/a: Jonathan Salgado 0 Comentarios. The value of a zero-coupon bond with a par value of 1 at time t and prevailing interest rate r is defined as: Since the interest rate r is always changing, we will rewrite the zero-coupon bond as: The interest rate r is a stochastic process that ... Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter There is another zero-coupon bond example if the face value is $4000 and the interest rate is 30%, and we are going to calculate the price of a zero-coupon bond that matures in 20 years. So, the under the given procedure will be applied to have the demanded answer easily: $4000 (1+.3)20; $4000; 190.049637748; $21.05

Advantages and Risks of Zero Coupon Treasury Bonds Perhaps the most familiar zero-coupon bonds for many investors are the old Series EE savings bonds, which were often given as gifts to small children. These bonds were popular because people could... Zero Coupon Bond Value - Formula (with Calculator) A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value. Understanding Zero Coupon Bonds - Part One The price for STRIPS with 25 years remaining to maturity would be $202.07 per $1,000 face amount That for STRIPS with 10 years remaining to maturity would be $527.47 per $1,000 face amount That for two-year STRIPS would be $879.91 per $1,000 face amount. Zero-Coupon Bonds: Definition, Formula, Example ... The price of zero-coupon bonds is calculated using the formula given below: See also Derivative Instruments - All You Need to Know Price = M / (1 + r) ^ n, where M = maturity value of the bond. (In other words, the face value of the bond) R = required rate of return (or interest rate) N = number of years till maturity

Price of a Zero coupon bond - Calculator - Finance pointers August 20, 2021. August 20, 2021. | 0 Comment | 9:15 pm. The Price of a zero coupon bond is calculated using the following formula : = FV / ( 1 + r ) n. Where. P = Price of a zero coupon bond ; FV = Face value / Maturity value of the zero coupon bond ; r = Discount rate ; n = Term to maturity ; In the calculator below insert the values of Face ... Zero Coupon Bond Definition and Example | Investing Answers The idea behind calculating the price of a zero coupon bond is so that you can determine the price you want to pay for the investment, based on the returns you want to earn. Example of a Zero Coupon Bond. Let's say you wanted to purchase a zero-coupon bond that has a $1,000 face value, with a maturity date three years from now. How to Buy Zero Coupon Bonds | Finance - Zacks The less you pay for a zero coupon bond, the higher the yield. A bond with a face value of $1,000 purchased for $600 will yield $400 at maturity. Zero coupon bonds are issued by the Treasury... The One-Minute Guide to Zero Coupon Bonds | FINRA.org will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000.

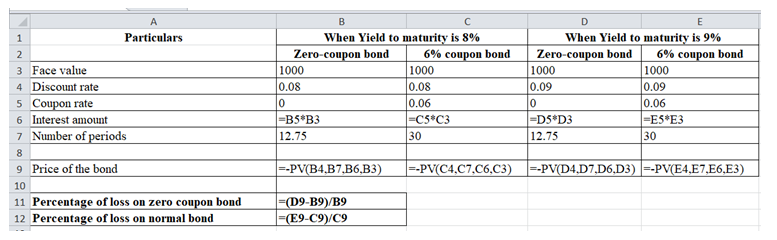

Answered: A 12.75-year maturity zero-coupon bond… | bartleby

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Bond valuation phd

Price of a zero coupon bond - Finance pointers Therefore the price of the zero coupon bond is = $ 5,000 / ( 1 + 0.06 ) 10 = $ 5,000 / ( 1.06 ) 10 = $ 5,000 / 1.790848 = $ 2,791.973885 = $ 2,791.97 ( when rounded off to two decimal places ) The price of the zero coupon bond = $ 2,791.97 Note : ( 1.06 ) 10 = 1.790848 is calculated using the excel function =POWER (Number,Power)

Current Price: Current Price Zero Coupon Bond

Should I Invest in Zero Coupon Bonds? | The Motley Fool Zero coupon bonds are therefore sold at a discount to their face value. So for instance, a 10-year zero coupon bond priced when prevailing yields were 3% would typically get auctioned for roughly ...

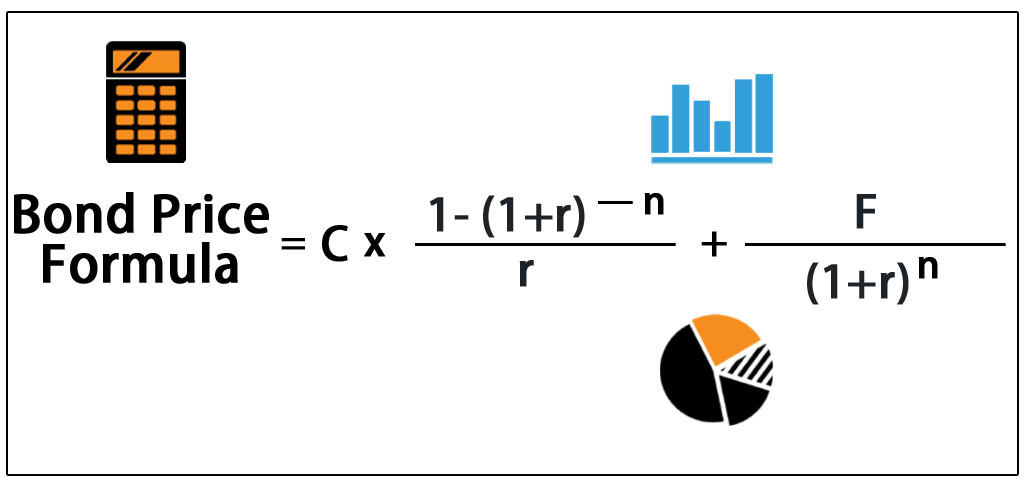

Bond Pricing Formula | How to Calculate Bond Price? | Examples

14.3 Accounting for Zero-Coupon Bonds - Financial Accounting This zero-coupon bond was sold for $2,200 below face value to provide interest to the buyer. Payment will be made in two years. The straight-line method simply recognizes interest of $1,100 per year ($2,200/2 years). Figure 14.11 December 31, Years One and Two—Interest on Zero-Coupon Bond at 6 Percent Rate—Straight-Line Method

Solved: An Investor Purchases A Zero Coupon Bond With 12 Y... | Chegg.com

Zero-Coupon Bond Definition - Investopedia If the debtor accepts this offer, the bond will be sold to the investor at $20,991 / $25,000 = 84% of the face value. Upon maturity, the investor gains $25,000 - $20,991 = $4,009, which translates...

PPT - Bond Pricing PowerPoint Presentation, free download - ID:391695

Zero Coupon Bond Value Calculator: Calculate Price, Yield ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

Zero Coupon Bonds - Zero Interest Rate Bonds - Citi Hong Kong

The Zero Coupon Bond: Pricing and Charactertistics ... This means if we pay something around $72 (100-28) on December 1, 1996 for the $100 coupon due on December 1, 2001, we will earn something around 30% over the period or 6% a year. Pulling out our trusty bond calculator, we can actually do the calculation. At a semi-annual yield of 5.6%, the price works out to be $75.91.

Post a Comment for "43 pricing zero coupon bonds"